Money flow doesn’t just move through your wallet — it’s the lifeblood of the entire economy. When the flow shifts, markets react, and business opportunities emerge or vanish. Driven by a willing-to-share passion to become informed, forward-thinking young individuals who stay ahead of the latest economic developments both locally and globally, we created this blog in order to share insights and build a valuable source of knowledge for our readers!

Gen Z meets a world in flux — will we catch up and lead the way? Along the way, can we make economics smart, sharp, and stylish?

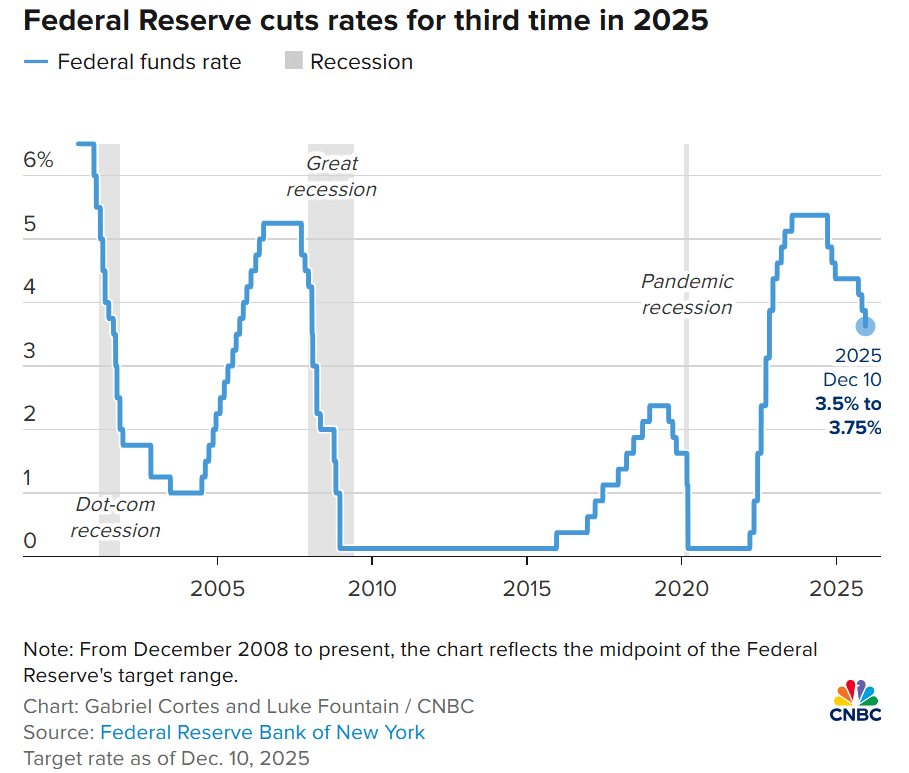

In its latest Federal Open Market Committee (FOMC) meeting (10/12/2025), the Fed further decreased the federal funds rate by 0.25 percentage points, cutting keys interest rate down to 3.50–3.75%. This marks the third consecutive rate cut in 2025 and the lowest level since November 2022. This move followed two tense days of meetings by FOMC, aimed at supporting economic growth and dealing with signs of job losses in the labour market. Remarkably, the Fed did not seek aggressive economic stimulus, but rather focused on adjustments to avoid a potentially deep recession.

US Federal Reserve Chairman Jerome Powell at a press conference.

“A further reduction in the policy rate at the December meeting is not a foregone conclusion—far from it,”

Powell said on October 29, the previous post-meeting press conference.

9-3 Vote – Hawkish and Dovish Dissents

Three FOMC members, a significant majority, oppose cutting interest rates. “Hawks are generally more concerned about inflation and favor higher rates while doves focus on supporting the labor market and want lower rates”, CNBC reported. This division shows that the Fed is in a phase of “risk reassessment,” no longer as clearly united as during previous crises. This disagreement also reflects concerns that inflation may not have truly cooled down sustainably, especially as service price indices remain at a high rate. “With today’s decision, we have lowered our policy rate three quarters of a percentage point over our last three meetings,” Jerome Powell concluded.

A “Tough” Signal for The Next Two Years

The closely watched “dot plot” of individual officials’ expectations on rates indicated only one cut per year for the next two years, by 25 basis points. After three interest rate cuts this year, officials have become more cautious about further rate reductions. They decided to stop to observe more and had not released any intention for January 2026. The market impact was also quite clear: US stocks increased slightly, gold prices rose, and the US dollar weakened after the decision. This demonstrates how markets react to changes in monetary policy, a key topic in finance and monetary studies.

“The discussions we have are as good as any we’ve had in my 14 years at the Fed, very thoughtful, respectful, and you just have people who have strong views, and we come together and we reach a place where we can make a decision,”

Artificial Intelligence is no longer a futuristic idea. It has moved from labs to daily life, from research papers to boardrooms, and from experiments to real economic impact. Over just a few years, AI has evolved into one of the strongest forces reshaping productivity, industries, business models, and the global workforce.

We are not witnessing a technological upgrade — we are living through an economic transformation.

Across industries, AI is becoming a core tool for boosting productivity and accelerating growth.

Repetitive tasks such as data processing, report generation, and basic analysis are being automated, freeing human talent for creative or strategic work.

Companies using AI in marketing, finance, logistics, and customer service report significantly higher output with fewer resources.

Entirely new industries and business models — from generative AI content services to smart healthcare — are emerging as AI becomes more integrated into the economy.

According to numerous global analyses, AI could contribute trillions of dollars to global GDP over the next decade. This positions AI not as a supporting technology, but as a major economic engine.

A Reshaping of the Job Market: Opportunities and Disruptions

However, alongside growth comes disruption — and the job market is feeling it first.

Jobs involving repetitive, rule-based, or predictable tasks are the most vulnerable.

The IMF estimates that up to 40% of jobs globally may be impacted by AI, with advanced economies experiencing the largest shift.

Workers in data entry, customer service, and basic content production face replacement risks, while highly skilled roles in AI engineering, cybersecurity, data science, and digital products are becoming more valuable than ever.

For developing nations, the threat is lower in the near term — but the pressure to adapt quickly is real. Individuals and economies that fail to reskill risk losing their competitive edge.

AI brings enormous potential, but also the possibility of deepening global inequities:

Countries with strong digital infrastructure and capital resources benefit more quickly than those still developing.

Large corporations, equipped with vast datasets and high computational power, are likely to dominate AI markets — raising concerns about monopoly power.

Creative industries face challenges around intellectual property, synthetic content, and fair compensation, as AI makes content production cheaper and faster.

Without thoughtful regulation and coordinated policy, the AI era could widen the gap between countries, companies, and workers.

Opportunities for Emerging Economies — Including Vietnam

For countries like Vietnam, AI presents both a challenge and a gateway to accelerated development.

Vietnam has growing potential in AI, semiconductors, and digital industries — sectors that could lift the country deeper into global value chains.

Local businesses adopting AI early gain a competitive edge through automation, smarter decision-making, and better customer experience.

With the right investment in digital skills, Vietnam’s workforce can transition into higher-value roles — instead of being displaced by automation.

This is a moment where smart national strategies can turn technological shifts into economic breakthroughs.

The future shaped by AI will be neither purely utopian nor dystopian — it will depend on the choices societies make today.

If managed well, AI can:

Boost productivity across every major sector

Improve healthcare, education, and public services

Unlock new industries and career paths

Help economies grow faster and smarter

But if left unchecked, AI may:

Concentrate wealth into the hands of a few

Replace vulnerable workers

Create new forms of inequality and digital divides

The world needs policies that support digital skills training, regulate AI ethics, and ensure fair opportunities for workers and businesses during this transition.

As Black Friday 2025 rolls in, one of America’s most iconic retailers may be leaving the spotlight for good. Once a retail powerhouse, Sears now faces what many analysts consider the final chapter of its holiday shopping season.

The reopened Sears store in Burbank, California, on December 1, 2023. While the store reopened that year, it closed once again in 2025, one of three Sears stores to close this year, leaving only five still operating. Samantha Delouya/CNN

From an Empire to a Few Stores

Just two decades ago, Sears operated thousands of stores nationwide. Following years of financial troubles — including a bankruptcy filing in 2018 — its footprint drastically shrank. Today, only five stores remain open across the United States.

Some of those remaining locations are reportedly under consideration to be sold or repurposed: for example, one store in Florida might be torn down to make way for new housing developments.

Why the Collapse Happened

Several factors contributed to Sears’ decline:

A shift in consumer habits: Shoppers increasingly favor online retailers or big-box stores offering lower prices and faster deliveries — trends that Sears failed to fully adapt to.

Financial missteps: Rather than investing in store renovation or e-commerce, management focused on selling real estate and buying back stock — a move many analysts say hastened the collapse.

Changing retail environment: With inflation, economic pressures, and fierce competition from modern retailers and online platforms, traditional department-store models have struggled globally.

A Sears store announces its closure in the city of Toronto, Ohio. Photo: Getty Images

What Black Friday 2025 Means for Sears — And Retail at Large

For long-time customers and former employees, this year’s Black Friday might mark more than a sales event — it could be a swan song. Experts suggest that even if the remaining stores survive through the holidays, chances are slim they will operate much longer.

Sears’ dramatic fall serves as a potent warning for other legacy retailers: in an era where convenience, adaptability, and digital presence reign, rest on past glory — and you risk disappearing.

Looking Ahead: What’s Next

With its shrinking footprint, repurposed stores, and declining consumer relevance, Sears may soon vanish from the retail landscape. Meanwhile, the holiday shopping season continues to be dominated by online giants and nimble competitors who better meet consumers where they are. For many, Sears will remain a nostalgic name — a reminder of a different era of shopping.

Central Vietnam is currently suffering severe flood damage. At least 41 people have died as of the 20th. Searches continue for 9 others who remain missing. This is extremely significant damage. As you can see in the photo below, the people in the lower left are waist-deep in water. In Japan, it’s extremely rare to experience flooding severe enough to reach waist level.

Even now, heavy rain continues to fall as recovery efforts are underway.

Why Central Vietnam Experiences Frequent Flooding

There are clear reasons why flooding occurs frequently in central Vietnam.

This is primarily due to the terrain. Mountains and the sea are close together, resulting in short rivers with steep gradients. This makes the rivers act like slides, rapidly pushing water downstream toward urban areas. Flooding occurs in the blink of an eye. Looking at the photos, you can see how close the riverbanks are.

Furthermore, this period coincides with the rainy season in central Vietnam.

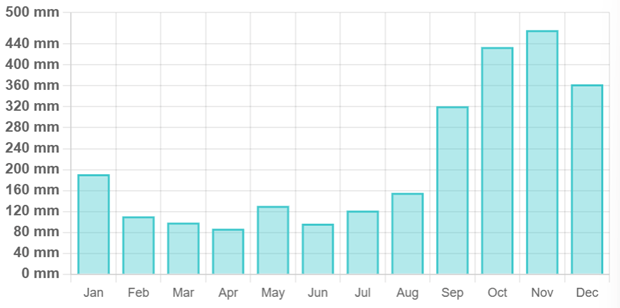

Annual precipitation in Da Nang

Specific Impacts on Vietnam’s Economy

Flooding of this magnitude will inevitably have a significant impact on Vietnam’s overall economic activity.

First, logistics across Vietnam will be disrupted. Vietnam is a long, narrow country stretching north to south. The central region is currently affected by the flooding. If major roads in the central region become impassable due to flooding and landslides, logistics will grind to a halt. When logistics stop, severe economic losses occur: raw materials and finished goods cannot be transported, and perishable goods spoil.

Next, factories flood, submerging and damaging expensive machinery and equipment. Even if factories themselves remain intact, surrounding roads may be flooded, preventing employees from commuting. Power outages halt operations, making work impossible. Without work, the economy grinds to a halt. Unfortunately, time doesn’t stop, meaning the economic losses during this period are immeasurable.

Finally, tourism significantly supports the economy of central Vietnam. However, flooding reduces the number of tourists. I believe the economy would develop further if the environment became more tourist-friendly. Yet, when typhoons strike, tour cancellations pile up, causing substantial economic losses.

The total economic loss from all these factors combined is estimated at approximately 358 million USD.

conclusion

I believe it is necessary to undertake river engineering projects for the mountainous regions to reinforce them and raise the embankments. While I understand these projects will require significant funding, I believe investing in them is more effective for the future, considering the substantial economic losses that will occur if central Vietnam continues to suffer flood damage for years to come.

Looking back at 2024, one of the most unforgettable moments for me, and for many Vietnamese, was the arrival of the Yagi Typhoon, the third major storm of the year. It wasn’t just another weather event. It was a wake-up call. I remember scrolling through news updates, watching videos of flooded streets, toppled trees, people of my country suffering, and thinking: “This is going to destroy more than homes. It’s going to destroy livelihoods.”

And it did.

The Immediate Shock:

When Yagi made landfall, it disrupted everything. Agriculture, logistics, tourism – sectors that are deeply woven into Vietnam’s economic fabric – were thrown off balance. Crops were destroyed, cattle were killed, houses were all “wiped” away. Farmers faced losses not just in produce but in future income, since Yagi had damaged infrastructure, cutting off supply chains and delaying exports, which means that all of their hard-work throughout the year, were all gone.

Tourism, which had been slowly recovering post-COVID, took a hit too. Coastal destinations saw cancellations, and various local businesses from homestays to seafood restaurants all struggled to stay afloat.

Watching this happen without being able to do anything about it really wrenched my heart.

Banana Crops in the river Hong (Ha Noi) were destroyed completely (Photo by Tran Cuong)

Economic Ripples:

The economic impact wasn’t just local. It rippled outward. According to reports, GDP growth projections were revised slightly downward for Q3 and Q4 of 2024. Manufacturing hubs in the south faced raw material shortages due to transport disruptions. Even the stock market reacted with caution, especially in sectors tied to agriculture and logistics.

But here’s the thing: Vietnam didn’t crumble. It adapted.

Turning Crisis into Motivation:

One of the most inspiring outcomes of Yagi was how it pushed both government and businesses to rethink resilience. Authorities accelerated infrastructure upgrades, especially in flood-prone areas. There was renewed interest in climate-adaptive agriculture like switching to flood-resistant rice strains and diversifying crops.

Digital transformation also got a boost. With physical supply chains disrupted, many SMEs turned to e-commerce and digital logistics platforms to stay connected with customers and suppliers. It wasn’t perfect, but it was progress.

I’ve seen many positive articles about how Vietnamese people bounced back immediately after such terrible crisis, that our people are incredibly resilient and will never give up.

Ha Long City had recovered from the Yagi Typhoon (Photo by Vu Bang)

Lessons for the Future:

Yagi was a harsh challenge for Vietnamese people, but it taught us valuable lessons:

Climate events are economic events. We can’t separate the two anymore.

Preparedness matters. Early warning systems, insurance coverage, and infrastructure investment are not optional. They are a must.

Innovation thrives in adversity. From digital pivots to community-driven solutions, Vietnam showed that creativity can be a survival tool.

So yes, Yagi was destructive. But it also sparked a deeper conversation about sustainability, adaptability, and economic resilience. And in that sense, it left behind more than broken roofs, it left behind a blueprint of a stronger future for Vietnam.

Sophisticated private sources could provide a fuller picture of the state of the economy. But the government is not even trying to use them.

Why Nobody Trusts Government Economic Data Anymore (And It’s Actually Getting Worse)

Here’s something that’s been bugging me lately: we’re living in the most data-rich era in human history, yet somehow, the government’s economic statistics feel less reliable than ever. It’s like having a smartphone in your pocket while your boss still insists on using a fax machine.

Last week really drove this home for me. The Bureau of Labor Statistics casually announced they’d miscounted jobs by—wait for it—911,000. That’s not a typo. Nearly a million jobs that supposedly existed just… didn’t.

Look, I get it. Revisions happen. But when your margin of error is bigger than the population of several states combined, we’ve got a problem.

So What’s Actually Going Wrong?

The cracks started showing years ago, but now they’re turning into canyons. Remember when you could actually get people to respond to surveys? Yeah, those days are gone.

Take the Current Population Survey, which is supposed to tell us about employment and demographics. Response rates have tanked from 88% in 2015 to just 68% today. Consumer spending surveys? Even worse—they’ve crashed from 68% all the way down to 40%.

Now here’s where it gets really messy: people aren’t refusing to participate randomly. Lower-income folks are dropping out faster than everyone else, which means official data is increasingly reflecting what’s happening with wealthier Americans. The Census Bureau quietly admitted that since 2020, they’ve been overstating median household income by about 2-3% because of this exact bias.

And honestly? I can’t blame people for not responding. If the administration is going to call government data “junk” anyway, why bother filling out another survey?

The Time Travel Problem

But wait, it gets better (or worse, depending on how you look at it).

By the time official economic data reaches policy makers, the economy has already moved on. The Fed’s big wealth survey? Conducted every three years, and results drop 18 months after they start collecting data. So the 2025 survey results won’t be available until late 2026. That’s basically ancient history in economic terms.

Think about that 2008 financial crisis for a second. The recession officially started in December 2007, but economists didn’t confirm it until December 2008. That’s a full year of economic pain before anyone in power officially acknowledged what was happening. By the time Congress passed stimulus in February 2009, we were 14 months into the crisis.

Could we have prevented some of that damage with faster, better data? Absolutely. But instead, we were flying blind.

The Real Kicker: We’re Starving the Data Agencies

You know what really gets me? While all this is happening, we’ve been systematically defunding the agencies responsible for collecting this information. Since 2009, statistical agencies have seen their budgets cut by 14% after adjusting for inflation.

The consequences are exactly what you’d expect. The Bureau of Economic Analysis stopped tracking self-employment by industry and county-level employment. The Bureau of Labor Statistics dropped price tracking for 350 product categories and cut back on Consumer Price Index data collection in multiple cities.

We’re essentially asking these agencies to do more with less, during a time when we need accurate data more than ever. It’s like telling a fire department to handle more emergencies with fewer firefighters and broken equipment.

The Irony That’s Driving Me Crazy

Meanwhile, hedge funds are making billions by tracking the economy in real-time using private data sources. They’re not waiting for government reports—they’re looking at:

Real-time payroll data from companies like ADP

Credit card transaction records (anonymized, of course)

Satellite images counting cars in Walmart parking lots

Redfin’s weekly housing market updates (which are apparently accurate to within 2% of actual sale prices)

During COVID, Harvard economist Raj Chetty built a dashboard using private data that tracked economic changes weeks before official government statistics caught up. It wasn’t some massive government project—just smart use of existing private-sector data.

So the technology exists. The data exists. We’re just… not using it.

The Pushback (And Why I Think It’s Overblown)

Now, government officials will tell you private data has problems—lack of transparency, potential bias, companies might change methodology or put data behind paywalls. And look, those are fair concerns.

But here’s my take: not using this data because it’s imperfect is like refusing to use GPS because paper maps are more reliable. Nothing’s perfect, but we need to be pragmatic here.

Research has already shown that combining official BLS numbers with ADP’s private payroll data actually reduces errors from both sources. It’s not about replacing government statistics—it’s about making them better.

What I Think We Should Actually Do

This shouldn’t be complicated or controversial. We need a hybrid system that:

Keeps doing traditional surveys for historical continuity and methodology, but integrates real-time private data that’s been properly vetted and documented. Then publish preliminary estimates using the private data, followed by refined numbers from traditional surveys later.

Most importantly, we need to properly fund statistical agencies so they can actually analyze and verify all this information.

Why This Actually Matters to You

I know this might sound like wonky economics stuff that doesn’t affect your daily life. But think about it: every decision about interest rates, unemployment benefits, stimulus checks, inflation adjustments to your salary—all of that depends on accurate economic data.

When the Fed raises interest rates based on flawed employment numbers, your mortgage gets more expensive. When stimulus arrives 14 months too late because we couldn’t detect a recession in time, that’s real families suffering unnecessarily.

We’re literally making trillion-dollar policy decisions based on information that’s months old and increasingly unreliable. That should worry everyone.

The Bottom Line

Right now, we’re living in an absurd situation where private investors have better, faster information about the American economy than the government officials making policy decisions that affect all of us.

The technology to fix this exists. The data exists. What we’re missing is the political will to actually modernize how we measure economic reality.

Until that changes, we’re basically driving into the future while staring in the rearview mirror—and we shouldn’t be surprised when we crash into things we didn’t see coming.

Understanding how energy shocks influence supply chains, costs, and competitiveness is essential for navigating the modern global economy.

The Reasons Behind EU’s Rising Energy Pressures

Europe, of 2025, is once again facing a serious energy challenge (since 2022) and fears of shortage. This situation is not happening in isolation, however, the whole world is feeling the pressure of unstable energy markets.

After years of global recovery from the historical pandemic and the war in Ukraine, many countries reduced gas production while demand kept growing. Unexpectedly cold winters in early 2025, led to an increasing in energy use for heating, while renewable sources, like wind and solar, couldn’t meet the full demand. At the same time, tensions in the Middle East and supply issues in Africa limited gas shipments to Europe. All these global factors combined to make the EU’s energy system vulnerable again.

When Europe faces an energy crunch, the rest of the world feels it too. Rising European demand pushes up global gas prices, affecting Asian and American markets. Developing countries that rely on imported energy now pay more, worsening inflation and slowing growth. For businesses, higher energy costs mean more expensive production, transportation, and materials everywhere — not just in Europe. Some European companies are even moving factories abroad to save costs, changing trade patterns worldwide.

Despite short-term difficulties, this crisis is both a warning and an opportunity. It has pushed Europe to accelerate its transition toward renewable energy. Investments in wind, solar, and green hydrogen are growing rapidly, supported by EU-wide initiatives to reduce dependence on imported fossil fuels. This shows that energy security and sustainability must go hand in hand. If Europe and other regions continue to invest in clean and reliable energy, these efforts could make the continent more energy-secure and environmentally sustainable in the next decade; therefore, the world can partly avoid similar shocks in the future.

Energy and Power icons set and grunge brush stroke. Energy generation and heavy industry relative image. Agriculture and transportation. Flag of the European Union

“Ensuring the security of energy supply remains a critical challenge for the European Union, particularly in light of Russia’s long-term weaponisation of energy, its war of aggression against Ukraine, the resulting geopolitical shifts, and the urgent need to diversify our energy sources while investing in domestic production” said lead MEP Beata Szydło (ECR, Poland).

The 100% Tariff: A New Line in the Sand for Protectionism

The latest developments in the US-China trade standoff are sending shockwaves across global markets. On October 10th, US President Donald Trump announced two extremely aggressive moves: a plan to impose 100% supplementary tariffs on imports from China starting November 1st, and the implementation of measures to control the use of US-made advanced software in China. Coupled with this was the possibility of canceling the scheduled APEC meeting with President Xi Jinping.

These announcements are more than just typical escalation; they signal a fundamental shift in the economic conflict between the two superpowers, evolving from a dispute over trade deficits to a strategic confrontation over technology and the global order.

Software Control: Elevating the Battle to the Tech Front

The measure controlling the use of advanced US software in China is arguably the most significant long-term strategic move.

The Goal of “Decoupling”: This action demonstrates the US’s determination to accelerate technological “decoupling,” especially in strategic sectors like artificial intelligence, semiconductors, and high-end manufacturing, where China still relies on US-designed technology and software.

Supply Chain Implications: This restriction will create major dislocations in the global technology supply chain, forcing multinational companies to build dual supply chains that are independent of China. This presents a historic opportunity for other nations, particularly manufacturing hubs in Southeast Asia.

President Trump’s statement about potentially canceling the APEC meeting is a concerning diplomatic signal.

Increased Instability: APEC is a critical forum for regional economic stabilization. Absence or tension there will increase instability and uncertainty in the markets, simultaneously weakening the multilateral trade order.

Economic Polarization: The move accelerates the process of nations being forced to “choose sides,” potentially leading to polarization into different economic blocs and slowing the pace of globalization.

As we can explain before, the US objective goes beyond merely balancing the trade deficit; it aims to contain China’s technological rise and alter its economic model. As long as the two powers maintain conflicting ambitions in shaping the global economic order, this rivalry will continue and become more multifaceted. Instead of an “end,” we are witnessing the formation of a new “economic cold war.”

As of October 14, the price of gold reached $4,127 per ounce, surpassing the $4,100 mark for the first time in history. This milestone represents a 56% increase compared to the same period last year, highlighting gold’s remarkable rally amid ongoing global uncertainties.

Several factors have contributed to the recent rally in gold prices:

Federal Reserve policy: The Fed’s recent signal of interest rate cuts has weakened the U.S. dollar, making gold — which is priced in dollars — more attractive to investors around the world. Lower interest rates significantly reduce the “opportunity cost” of holding gold—a non-yielding asset—as it becomes less attractive to park money in interest-bearing assets like bonds.

Inflation concerns: With inflation expected to stay elevated for an extended period, investors are increasingly seeking protection against the erosion of purchasing power. As consumer prices rise and real interest rates remain low or negative, the appeal of holding gold as a means to preserve wealth has strengthened considerably.

Geopolitical instability: Ongoing conflicts and political tensions, including recent drone and missile attacks in Ukraine, have further driven demand for traditional safe assets like gold as global risk sentiment worsens.

Analysis and Outlook

“Gold could easily continue its upward momentum. We could see prices north of $5,000 by the end of 2026,” stated Phillip Streible, Chief Market Strategist at Blue Line Futures.

In the short term, analysts expect gold prices to fluctuate within the $4,000–$4,200 range, as traders balance optimism about rate cuts with caution over short-term profit-taking.

Over the longer term, the outlook remains positive. If global economic uncertainty persists and central banks maintain an easing bias, gold could sustain its strong performance as investors continue to seek stability and diversification.

With cashless payments becoming widespread these days, are you using such convenient payment methods? I don’t use them much myself, as I’m not familiar with any cashless payment methods in Vietnam besides credit card payments. However, I see many people using cashless payments. I believe this convenience is influencing your consumption behavior.

First, psychology has a term called the “pain of paying.” This refers to the phenomenon where the act of actually paying money to purchase goods or services causes psychological pain or discomfort for us consumers, much like the “pain of feeling your wallet get lighter.” The degree of this “pain” varies significantly depending on the payment method, timing, and the size of the amount. (1) In other words, the absence of physical cash exchange makes even large payments feel minor. For example, wouldn’t you agree that cashless payments feel more convenient than counting out 1000k (VND) in cash? This phenomenon is called the “pain of paying.”

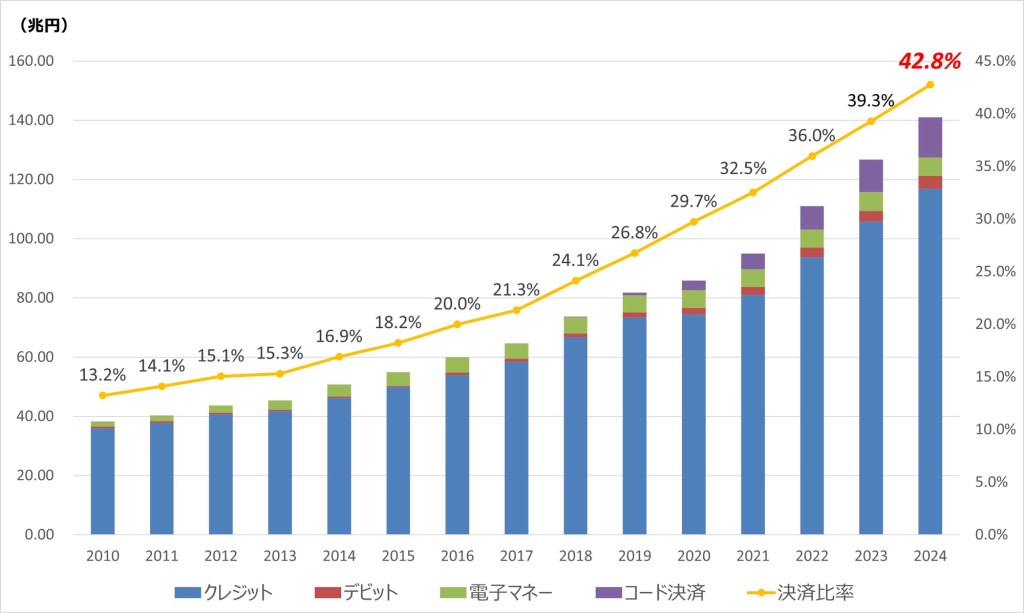

Trends in Japan’s Cashless Payment Amounts and Ratios (2024)

Next, here is a graph showing cashless payment amounts based on a survey by Japan’s Ministry of Economy, Trade and Industry. (2) In 2016, it was 20%, and in 2024, it reached 42.8%. We can see it has nearly doubled. This indicates that cashless payments are becoming more widely used, and people are spending significantly more money.

Finally, let’s touch on the benefits brought by the spread of cashless payments. They significantly contribute to reducing labor costs. This is because they eliminate the hassle of closing out registers and preparing change. Additionally, they cut costs associated with transporting cash. Since cashless transactions are recorded, manual calculation errors decrease. Furthermore, electronic coupons are easier to use. People tend to let paper coupons expire, but electronic coupons can be used casually. If cashless payments become more widespread, cash-related crimes will decrease. This is because as more people stop carrying cash, fewer people will commit robbery or theft. There are many benefits like this. However, I also considered the drawbacks. If cyberattacks or data breaches occur, can we truly say cashless payments are secure? If it happens, it would be frightening. Additionally, if a disaster strikes, could we, who depend on this system, survive without cash? In today’s world, it’s wise to carry cash alongside using cashless payments.

Considering the psychological concept of “pain of paying” discussed above, and the fact that cashless payment amounts are rising, we should exercise caution when using convenient cashless payment methods.